Articles by

Janine Mace

-

Worried about your retirement savings? 9 steps that can help

Worrying about whether your retirement savings will be enough is normal, but there are some easy steps you can take to ensure you’re as prepared as you can be for retirement.

-

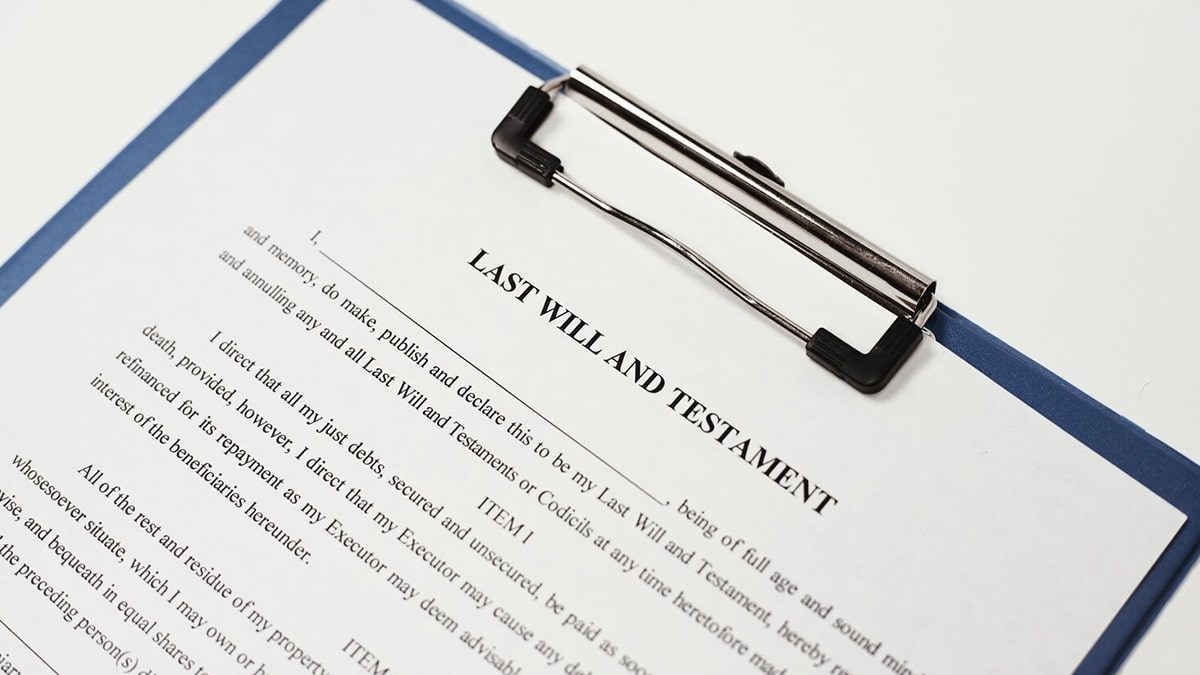

SMSFs and estate planning: What it is and why it matters

Along with a valid Will, your SMSF is an essential part of your estate plan. From your personal wishes to tax and legal matters, there’s a lot to consider.

-

What is a testamentary trust and does my Will need one?

Establishing a testamentary trust can have valuable estate planning benefits. With significant amounts due to be transferred via inheritances in the coming decades, it may be worth considering one.

-

Insurance in super: What to know and how to manage your cover

If you have insurance inside super but you’re not sure how it works, it’s easy to take control once you learn the basics and how to assess your needs.

-

How redundancy and retirement impact your employees’ super

Working out termination and super payments for a departing employee can be confusing, but be careful not to provide them with financial advice.

-

10/30/60 rule: How investment returns shape your retirement income

The investment return on your super pension account is just as important as the returns you earn on your super while you are working, as this simple ‘rule of thumb’ demonstrates.

-

Unlisted assets: What are they and why is my super fund investing in them?

Unlisted assets are an important investment for some larger super funds as their more stable returns provide a useful balance for the volatility of listed assets like shares.

-

Strategies for boosting your super in the gig economy

While working in the gig economy can be more flexible, it can also be a recipe for a much smaller retirement savings pot if you don’t take steps to fix it.

-

Why super funds diversify and what you can learn from it

Diversification is one of the key principles behind good investing and there’s a lot you can learn from how successful super funds invest their members’ money.

-

What are defined benefit super funds?

Although defined benefit funds are disappearing in Australia, if you’re lucky enough to be a member, they can offer a valuable way to save for your retirement.

-

SMSF estate and succession planning: What’s the difference?

When planning who gets what when you die, many people forget about their SMSF. It’s not just about the distribution of fund assets, but who’s in control.

-

Had enough of your SMSF: What are your options?

Running an SMSF can sound appealing when you start out, but as the years pass there are many reasons you may want out. So, what are the alternatives?

-

How your super fund works and who’s who in your fund

Ever wondered why your super fund is set up like it is, or who provides all the services to members? We have the simple answers to all your questions.

-

Revamp for super system: Financial Services Royal Commission recommends change

The final report from the Royal Commission is likely to result in major change for the superannuation industry – both for super fund members and for trustees and executives managing the large super funds.

-

Super’s next shake up? Productivity Commission gets tough

Australia’s current super system is “harming millions of members” through underperforming funds, multiple accounts and excessive fees.